How do you know when the price is “right”?

Think about the last time you went shopping. What were you shopping for? Clothes? New athletic shoes? A birthday gift for a friend? Whatever it was, you probably found a lot to choose from. Athletic shoes, for example, come in dozens of styles and brand names. In the end, how did you decide what to buy? If you are like most consumers, price was an important component of your decision, perhaps even the deciding factor.

As consumers, most of us think of prices simply as indicators of what we have to pay to get what we want. Economists see prices differently. Looking at prices from the point of view of an economist, we find that they perform a number of important roles in a modern mixed economy.

A primary role of price is to convey information. Both consumers and producers use this information to help make decisions. It may be an overstatement to call prices a “language.” but prices do send a signal. The high price of Manhattan real estate. for example. signals that this particular good is in short supply. The low price of rubber flip-flops sends the opposite signal. As economist Thomas Sowell puts it, “Prices are like messengers conveying news.”

To consumers. price signals the opportunity cost of a purchase. The opportunity cost of buying any product, remember, is the next best use for the money you spend. You may not think twice about buying something inexpensive. like a pack of shoelaces. because you give up little opportunity with the dollar you spend. On the other hand. before buying a pricey item like a flat-screen television, you would probably shop around. research brands. and seek out the lowest price. When the opportunity cost of buying is high. people tend to think carefully before parting with their money.

Prices convey information to producers as well. Prices tell producers what consumers want. Auto mobile manufacturers. for example. pay attention to which models and features sell at high prices and which need to be marked down in order to attract buyers. Prices are a way for automakers to gauge consumer preferences. Without monitoring prices, carmakers wouldn’t know which models to produce more of and which to cut back on.

Producers also use prices to appeal to the consumers they hope will buy their products. A firm that produces backpacks. for example. might offer a stylish model at a low price. targeted to preteens who want packs for school. The same firm might produce heavy-duty backpacks for serious adult hikers and offer them at higher prices. In each case. price sends a message about products and their intended markets.

Consumers, for their part, are used to interpreting these messages. They know that producers are trying to appeal to a wide range of tastes and budgets. Consumers use price to sort through the resulting variety of goods in the marketplace. Faced with a vast selection of running shoes ranging in price from around $l9 to over $200. for example. most consumers will narrow their searches to a limited price range. The choice of how much to spend may. in part be based on what a person can afford. but it also reflects the consumer’s expectation of what will be available at that price.

As the incentives-matter principle reminds us. people respond to incentives. In a market-based economy, prices function as an incentive because they represent potential for profit. Rising prices in a market motivate existing firms to produce more. and they encourage new firms to enter the market. Falling prices. in turn, serve as incentives for firms to cut back on production or even to leave a market to look for better opportunities elsewhere.

When home prices increase. for example. the change signals construction firms. architects. builders. and tradespeople that there are profits to be made in the housing market. Existing firms build more houses, and new firms get into the act. When prices in the same housing market decrease, the reverse happens. Construction firms build fewer houses. Architects. builders. and tradespeople look for other markets for their talents. such as house renovations and commercial construction.

lust as changing prices motivate producers. prices in the form of wages and salaries motivate workers. The opportunity to earn a higher “price” can inspire people to enter the workforce or seek higher-paying jobs. On the other hand. low wages can act as disincentives for people to seek work.

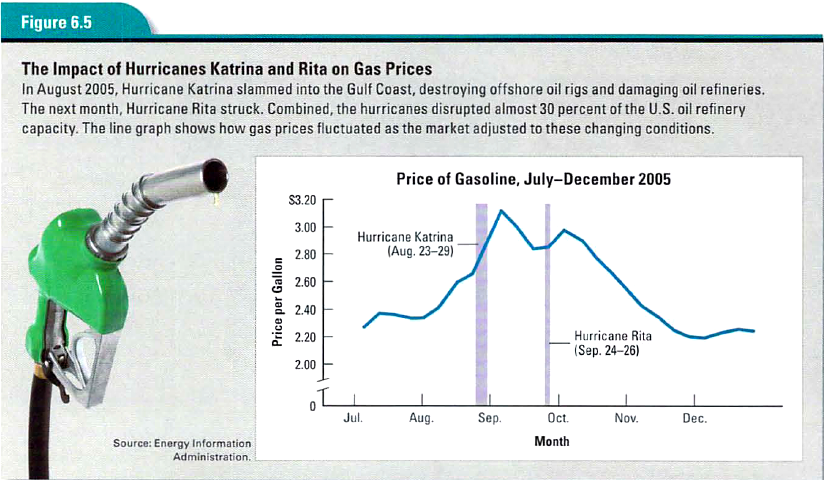

Prices allow markets to adjust quickly when major events such as wars and natural disasters interfere with the production or movement of goods. wreaking havoc on supply. Figure 6.5 shows what happened to gas prices in late summer 2005. when the U.S. Gulf Coast was slammed by two powerful hurricanes. The first. Hurricane Katrina, shut down most crude oil production in the Gulfof Mexico and damaged oil refineries from Texas to Florida. Immediately afterward. a government official described the uncertainty facing the oil industry.

Four weeks later. just as the industry was starting to recover. Hurricane Rita struck. causing additional disruptions to the oil supply. The two hurricanes brought a halt to almost 30 percent of the U.S. oil refinery capacity.

For the next few weeks. gas prices fluctuated. sometimes wildly. as oil companies struggled to bring the quantity of gas demanded in line with what refiners were able to supply. One newspaper reported. “Confused drivers in Georgia saw prices that had climbed as high as $5 a gallon suddenly drop back to $3 in the span of 24 hours.” Fluctuating prices frustrated consumers. but they allowed the market to adjust to the disruption in supply caused by the hurricanes.

By early November 2005, the industry had largely recovered. with only 5 percent of Oil-refining capacity still disabled. The retail price of gasoline that month averaged $2.30 per gallon. A month later, the average price had dropped to $2.23 per gallon. lower than it had been before Hurricane Katrina. This new, low equilibrium price reflected the fact that in addition to the increase in supply as U.S. facilities went back on line. refiners throughout the world had rushed fuel to the United States in the months after the hurricanes. As the supply of gasoline increased. prices at the pump went down.

By throwing the gasoline market into disequilibrium, Hurricanes Katrina and Rita illustrated the key role that prices play ill correcting both shortages and surpluses. Prices give markets the flexibility they need to reach equilibrium even under changing conditions.

Perhaps the most important role of price in a market-based economy is to guide resources to their most efficient uses. Consider, for example. the market for dairy products, such as yogurt. ice cream, and cheese. The firms whose dairy products are in greatest demand will buy the most milk in order to make products to meet that demand. Guided by prices that communicate what consumers want, dairy producers automatically allocate milk — a scarce resource used to make many different products — to its most valued use.

Or consider the earlier example of car manufacturers who use prices to decide which models to produce and in what quantities. These production decisions are. at bottom. decisions about how best to use limited resources. As Thomas Sowell explains,

{kind=link}