How do you know when the price is “right”?

Economists think of the equilibrium price as the “right” price because it is the price that producers and consumers can agree on. Sometimes, however, producers set a market price that is above or below the equilibrium price. Economists refer to this state of affairs as disequilibrium. When disequilibrium occurs in a market, the quantity demanded is no longer equal to the quantity supplied. The result is either a shortage or a surplus.

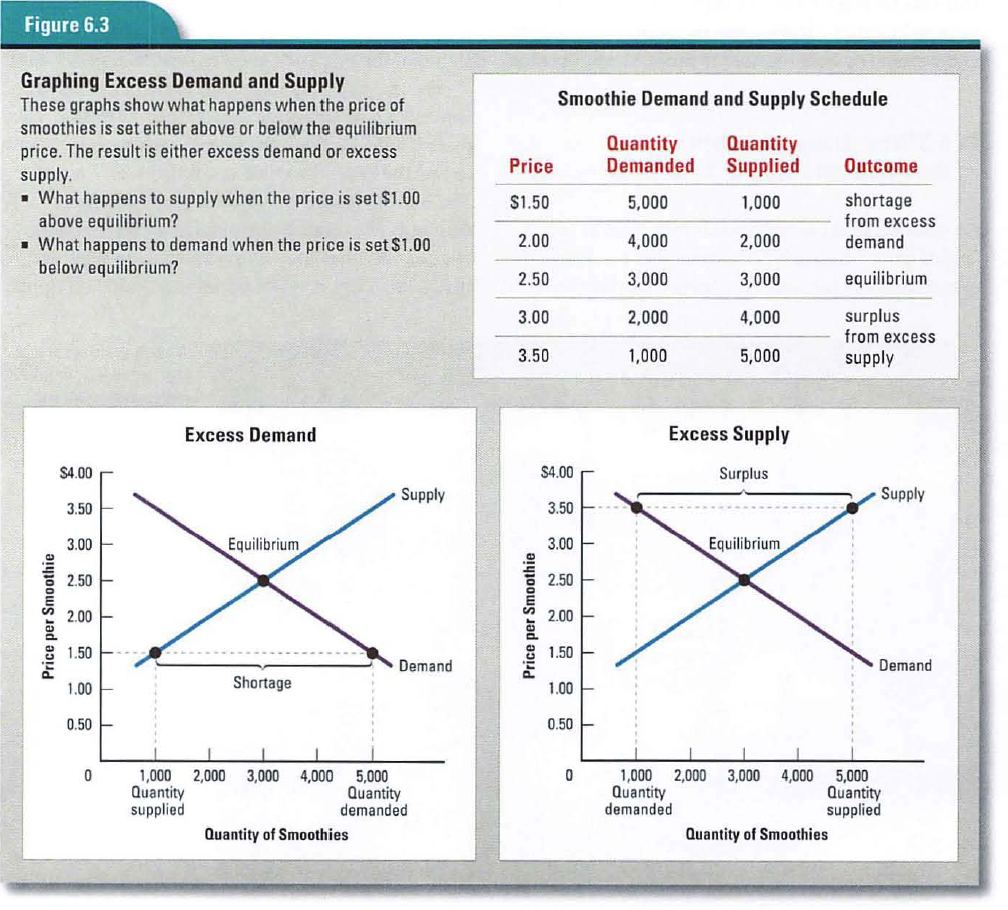

Have you ever stood in a long line waiting for the latest video game release? Or have you gone to a theater to see a blockbuster movie only to find the tickets sold out?

Economists call situations like these — in which the quantity demanded at a specific price exceeds the quantity supplied — excess demand. Consumers experience excess demand as a shortage. A shortage occurs when there are too many consumers chasing too few goods. To economists, excess demand is a sign that the price of a good or service is set too low. For example, suppose the owners of a juice bar concoct a new smoothie called Blueberry Blast. They price it at $1.50. Soon the line of customers waiting to buy the $1.50 smoothie is out the door, every day.

The owners realize they have a problem — excess demand. The quantity demanded greatly exceeds the quantity they are willing and able to supply at this price. They may not be able to afford additional staff to accommodate all the customers, or to pay for all the smoothie supplies. The low price results in reduced profits for the owners.

The first graph in Figure 6.3 illustrates this problem. At $1.50 per smoothie, customers will buy 5,000 drinks per month. The juice bar owners supply only 1,000 smoot hies at this price. The result is a shortage for the many customers who want smoothies and are not able to buy them.

The juice bar owners could solve their excess demand problem by increasing the price of their smoothies until they have fewer long lines throughout the day. Doing this would bring them closer to the equilibrium price, at which the quantity demanded equals the quantity supplied.

Have you ever looked through a clearance rack for bargains on clothes? Or have you looked for laptops or cell phones on a Web site that sells overstocked electronic goods? These marked-down products have something in common. They were all initially offered for sale at prices above what consumers were willing to pay. The result was excess supply, a situation in which the quantity supplied at a specific price exceeds the quantity demanded. Producers experience excess supply as a surplus. A surplus occurs when there are too few consumers willing to pay what producers are asking for their goods.

Suppose that the juice bar owners, in trying to solve their excess demand problem, raise the price of a Blueberry Blast to $3.50 per drink. Business slows, and they soon discover that they are not selling enough drinks. The quantity demanded by customers is much less than the quantity the juice bar owners want to supply at this price. The excess supply results in a surplus of blueberry smoothie ingredients. Boxes of fresh blueberries go bad in the refrigerator and blenders stand idle on the counter.

The second graph in Figure 6.3 shows that at $3.50 per smoothie, the juice bar owners are willing and able to produce 5,000 drinks. But customers buy only 1,000 smoothies, resulting in a surplus. If the owners choose to reduce the price. more customers would be willing and able to buy. The price would then move toward the equilibrium price, at which quantity demanded equals quantity supplied.

What price should the juice bar owners set for their Blueberry Blast? Figure 6.3 shows that the “right” price is $2.50. At that price, the quantity of smoothies demanded — 3,000 — equals the quantity supplied.

In a free market, surpluses and shortages are usually temporary. When a market is in disequilibrium, the actions of many producers and consumers serve to move the market price toward equilibrium. How long it takes to restore the equilibrium price varies from market to market.

Owners of a local juice bar might be able to change their blueberry smoot hie prices every month until the price is “right.” In contrast, a national fast-food chain might take much longer to find the “right” price for every item on its menu. Menus, signs, and advertising would need to be changed for all the many restaurants. Whether prices change quickly or slowly, however, once they move toward equilibrium, shortages and surpluses start to disappear.

{kind=link}