Why can't you always get what you want?

Some decisions in life are easy. You probably don’t fret much over which option to choose from a school lunch menu. Other decisions are agonizing. Think back to the choice facing Mick Jagger when he realized he did not have enough time to both continue his studies and be the lead singer in a band. It was “very, very difficult,” he said later, because his parents wanted him to stay in college. But there was another reason this decision was so tough. In making his choice, Jagger had to give up something he valued (education) to get something he valued even more (a chance to become a rock star).

The way economists see the world, people seek to make themselves as well off as possible by maximizing the utility of their decisions. They usually define utility as the satisfaction or pleasure one gains from consuming a product or service or from taking an action. But utility is more than that. We also gain utility by making choices that, while not all that pleasurable, are likely to improve our lives. Getting a vaccination or studying for a test may not be your idea of fun, but both should make you better off in the long run.

Maximizing utility is seldom easy. Whether choosing which television program to watch or which college to attend, we seldom have enough information to be absolutely sure we have made the best choice. This was true for Mick Jagger as well. When choosing between school and music, he had no way of knowing how successful the Rolling Stones would become. Nonetheless, he made the best judgment he could about the utility of one alternative over the other. In retrospect, he seems to have gotten it right.

As the scarcity-forces-tradeoffs principle reminds us, every decision we make-even one as simple as deciding to read this book-involves giving up one thing for another. To gain time to read, you are giving up all of the other things you could be doing right now. Each of those alternatives not chosen is a tradeoff.

Like individuals, businesses face tradeoffs as they try to maximize the utility of their land, labor, and capital. Suppose an automaker decided that it could best use all of its factories and workers to build pickup trucks instead of cars. The tradeoff of its decision would be the loss of its passenger car business.

Societies face tradeoffs as well. The classic example used by economists is the guns-versus-butter tradeoff, in which a society must choose between using its resources to produce guns (military goods) or butter (civilian goods). If the society chooses guns, it maximizes its security, but at the cost of lowering living standards. If it chooses butter, the society maximizes living standards, but at the cost of reducing security.

You may have noticed that each decision made by a society in the guns-versus-butter example involved a cost. The same is true for the decisions you make. When you choose one course of action, you lose the utility, or benefits, of the alternatives you did not choose. Were you to rank those alternatives, one would likely stand out as more attractive than the rest. While you might think of this option as your second-best choice, an economist would see it as your opportunity cost.

The opportunity cost of any action is the value of the next best alternative that you could have chosen instead. Whether you have 2 alternatives or 200, your opportunity cost is simply the value of the next best one. Think back to Mick Jagger’s decision. His opportunity cost of pursuing a singing career was the future utility of the college degree he never earned. Similarly, the opportunity cost of the automobile company that decided to produce only trucks was the money it would have made by continuing to produce cars.

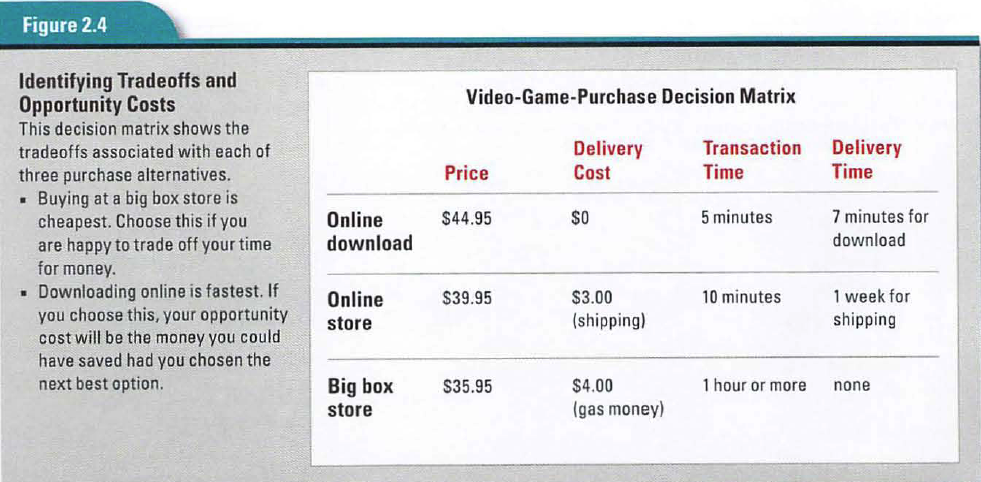

Understanding the opportunity costs of the choices you face every day can help you make better decisions. Put yourself in this situation. There is a new video game you want to buy. You can download the game from an online store for $49.95. You can order the game CD from a computer catalog for $42.95 plus $3.00 shipping, but it will take at least a week to get to your home, or you can buy it today for only $35.95 at a big box store in a nearby town, but it will take an hour of your time and about $4.00 of gas to drive there and back.

One way to sort through these alternatives is to lay them out on a decision matrix like the one in Figure 2.4. The matrix lists all the alternatives involved in the decision as well as the criteria, or factors, that might be used in evaluating those alternatives. In this instance, the factors are price, delivery cost, transaction time (how long it will take you to complete the purchase), and delivery time. The decision matrix doesn’t tell you which alternative to choose, but it does clarify what you will gain and lose by choosing one over another.

After analyzing the alternatives, you decide you really want to buy the game today. If you choose to download it from the online store, your opportunity cost is the $10 you would have saved by driving to the big box store. If you choose to buy it from the store, your opportunity cost is the hour you would have saved by downloading the game.

Knowing the opportunity cost of each alternative still does not tell you what to do. That depends on the value of $10 or an hour’s time to you. Should you have a better use for that hour, such as working at a job that pays $15 an hour, you probably would be better off downloading the game. If not, you might decide that trading an hour of your time for a savings of $10 is the better choice.

Note that in the video-game-purchase scenario, you were not facing an all-or-nothing, “buy the game or do without” decision. Instead, you were employing the thinking-at-the-margin principle by looking at the marginal utility of one purchase alternative over another. Marginal utility is the extra satisfaction or pleasure you will get from an increase of one additional unit of a good or service. One alternative in the scenario left you with more time compared to the others. Another left you with more money.

An understanding of marginal utility begins with the recognition that the amount of satisfaction we get from something usually depends on how much of that something we already have. Suppose you are so thirsty after a workout that you buy yourself a large bottle of apple juice. The first glass provides you with a high level of utility by quenching your thirst. The second glass is still satisfying, but its marginal utility is less because you are no longer so thirsty. The third or fourth glass has less utility as your thirst disappears and your stomach fills up. The fifth glass, should you go on drinking, might have a negative utility by making you feel sick.

As this example shows, the marginal utility of something diminishes as we get more of it. This explains why a homeless person is more likely to pick up a dollar bill off the sidewalk than a millionaire is. The dollar has a relatively high marginal utility to a person with little money. Conversely, the marginal utility of an extra buck to a person who already has a million dollars is relatively low. An economist would see this difference in behavior as an example of the law of diminishing marginal utility. According to this law, as the quantity of a good consumed increases, the marginal utility of each additional unit decreases.

Most of the choices we face every day are “how much” decisions at the margin. Think back to the video game example. How much more would you be willing to pay to' get the game right now? How much longer would you be willing to wait to get the game for less? Whenever you find yourself asking “how much” questions like these while considering a choice, you are thinking at the margin.

{kind=link}