How should you spend, save, and invest your money?

Thirty years ago, Americans saved more of their incomes than they do today. Economists know this by measuring Americans’ personal saving rate — the proportion of a household’s income that its members save each year.

Figure 8.4A shows that in the early 1980s, the personal savings rate often topped 10 percent. By 2013, it had fallen to about 4 percent. That means the average American household is setting aside almost none of its income for the proverbial rainy day. Should we be concerned about our general lack of thrift? Does the future-consequences-count principle matter when it comes to saving?

The money you and others set aside in savings accounts, retirement plans, and other forms of saving is not just important to you personally. It also contributes to the nation’s overall economic growth.

How does this work? Personal savings provide funds that banks can lend to businesses for expansion — what economists call investment in capital goods. When businesses invest in capital goods, the economy grows. For example, suppose a company borrows money to build a new factory. The new factory increases the company’s output. More goods are produced and sold, creating growth in the economy.

Building a factory also generates growth indirectly. It provides revenue to a host of other producers, from construction companies to equipment suppliers. Those producers can then launch their own expansions. A new factory also creates jobs. The workers’ wages flow to local businesses. Wages also flow into the bank accounts of the workers themselves. Banks use these deposits to start another round of lending and even more economic growth.

To most Americans, the idea of saving money is less exciting than the idea of spending it. As our personal saving rate suggests, we are a nation of consumers. Saving part of one’s income, however, does not mean never consuming it. In fact, some economists define saving as “consuming less now in order to consume more in the future.” We all have goals for the future. Perhaps your goal is to become a lawyer. an engineer. or a teacher. To do that you will need a college degree. Maybe your goal is to buy your own car or house. Maybe you dream of traveling the world or starting a business. Whatever your goal, it is likely to require money. Setting aside a portion of your income now to cover later expenses is saving for the future.

Do you know anyone who lived through the Great Depression? That person could tell you about hard times — businesses ruined, homes and life savings lost, few jobs, and little hope. The Depression affected nearly everyone in the United States to some degree.

Even when the economy is strong overall, financial misfortune can strike at any time — when a company lays off workers, when a business fails, or when a family gets hit with huge medical bills. Such events often come unexpectedly. Unless you are ready, you could find yourself facing real financial hardship.

To be prepared for a financial emergency, experts advise building up a “rainy-day fund” — an easily accessible stockpile of savings. Most advisers say your fund should contain at least six months’ worth of salary. Others suggest that $2,000 to $3,000 is enough as long as you also have insurance to cover catastrophes. All experts agree, however, that a rainy-day fund should be used only for real emergencies. As financial adviser David Bach observes,

Have you ever considered what you will live on when you retire? At this point in your life, that question must seem like a remote concern. “First,” you might answer, “let me finish my education and choose a career.”

Retirement is indeed a long way off. But in just a few years you will likely be working full time — earning, spending, and, if you are wise, saving. If you are really looking ahead, you will be saving for your eventual retirement.

Americans today are living longer than ever before. Many people starting careers today will live for 20 or more years after they stop earning a paycheck. To maintain even a modest lifestyle during those years will take a lot of money. The earlier you begin accumulating that money, the more you will have when the time comes to retire.

Most retired people support themselves using three sources of money, making retirement something like a three-legged stool. The three “legs” are Social Security, company retirement plans, and personal savings.

Social Security. Social Security is a government program that provides cash payments to retired workers. It is funded by taxes paid by workers and their employers. Social Security is a pay-as-you-go plan. This means that the Social Security taxes you pay each year are not saved for your future retirement. Instead, this money is paid out in benefits to current retirees.

Company retirement plans. At one time, most large companies offered pension plans to their employees. A pension plan is a retirement plan to which the employer makes contributions for the future benefit of its employees.

Today the most common company retirement plan is the 401(k) plan. This plan gets its name from section 401(k) of the Internal Revenue Code — the main body of our nation’s tax laws. In a 401(k) plan, employees have money automatically taken out of their paychecks and put into retirement investment accounts. Employers may also contribute to the plan by matching all or part of an employee’s contribution.

One benefit of a 401(k) plan is that participants may subtract their contributions from their taxable income when they file their tax returns. The effect is to lower the amount of income tax they are required to pay. Financial experts encourage all employees to put money into a 401(k) if their employer offers such a plan.

Personal savings. The third source of retirement funds is personal savings. Such savings may include a variety of financial assets, including private retirement plans — plans that are not employer-sponsored.

An Individual Retirement Account is a private retirement plan sponsored by the federal government. Anyone who earns income can put money into an IRA. To encourage Americans to do so, the government has built tax advantages into IRA plans. Depending on the type of plan they choose, participants may either deduct the amount of their IRA contributions from their taxable incomes or take money out of their accounts tax free when they retire. For this reason IRAs are often referred to as tax-sheltered savings accounts.

IRAs, pensions, and other retirement plans come in many forms, each with its own set of rules. These rules govern such things as the amount you can contribute each year, how the account is taxed, and when you can begin to withdraw money from the account. Retirement savers should choose the plan that best suits their circumstances and meets their long-term goals.

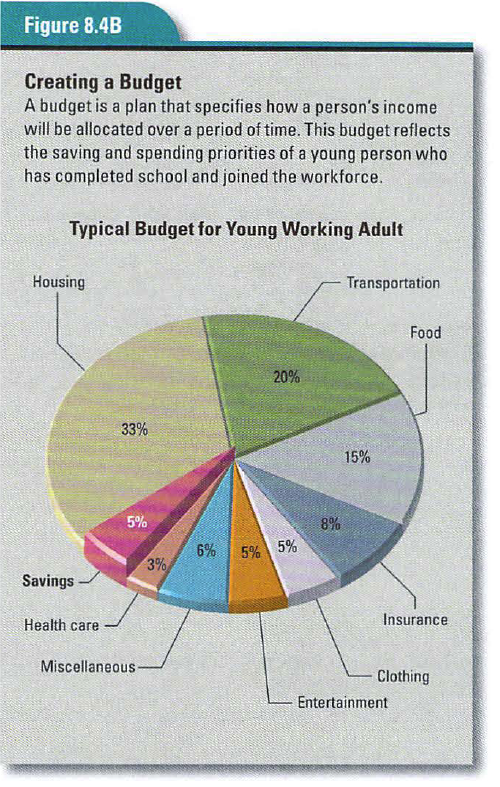

A budget is a plan for spending and saving, based on one’s income and estimated expenses. It covers a specific time period, typically a month or year. For those who really want to take control of their day-to-day finances, making a budget is essential.

The first step in creating a budget is to estimate your monthly income and expenses. This means keeping track of all income as well as all expenditures for a month. Figure 8.4B shows a typical budget for a young adult. It includes a mortgage or rent payment, a car loan payment or transportation expenses, as well as food, clothing, and other items.

When most people construct a budget, they make the mistake of calculating only the cost of goods and services consumed. They subtract those expenses from their income, and what is left — if anything — goes toward savings.

To become a successful saver, however, saving needs to be an entry in your budget right from the beginning — perhaps even your first budget item. Setting aside money each month as savings might be difficult, but the effort will be well worth it. Nothing could be more important to your financial future.

{kind=link}